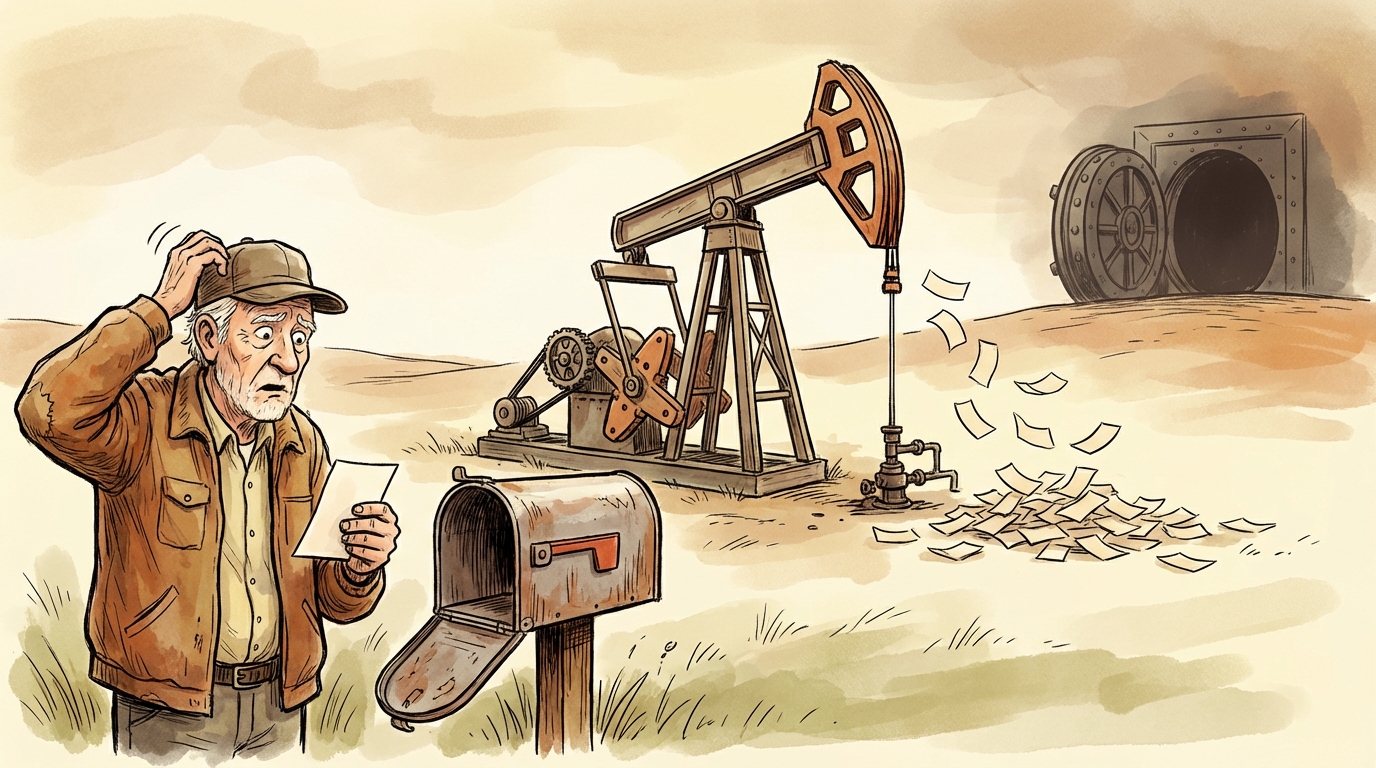

You did everything right. Your grandfather leased the family land decades ago. The operator drilled a successful well. The oil is flowing out of the ground, and for a while, the checks arrived in your mailbox every month like clockwork.

Then one day, the checks just stop.

You call the operator. They tell you they are doing their job perfectly. The well is pumping. The oil is going into the pipeline. But the company buying the oil out of that pipeline just filed for Chapter 11 bankruptcy.

You assume your money is safe. After all, it is your oil. The lease says you get a percentage of the proceeds.

Bankruptcy court disagrees. The judge bangs a gavel and tells you that you do not own the oil anymore. You are now just another :unsecured creditor standing in line behind massive Wall Street banks, hoping to collect pennies on the dollar.

This is the nightmare scenario for mineral owners. We talk to families all the time who think their only risk is a dry hole or a drop in the price of crude. But the real structural danger often lies with a counterparty you never even signed a contract with.

Let’s look at what actually happens when the middleman goes broke.

The $2.4 Billion Casino

Back in 2008, a midstream company called SemGroup L.P. was buying crude oil from thousands of wells across Texas, Oklahoma, and Kansas. They were massive. The year before they collapsed, they had revenues of $13.2 billion. If you owned minerals in the mid-continent, there was a good chance SemGroup or its subsidiary, SemCrude, was the :first purchaser picking up your oil.

SemGroup was supposed to be a boring pipeline and logistics company. They buy oil at the wellhead, move it, and sell it to refineries downstream.

But they got greedy. They started trading financial options contracts on the NYMEX. They were betting massive amounts of money on the future price of oil. When the market turned against them, they lost $2.4 billion.

SemGroup collapsed into bankruptcy. At that exact moment, they held millions of dollars in crude oil they had taken from the wellheads but hadn’t paid for yet. Thousands of mom-and-pop mineral owners and independent operators suddenly realized their royalty money was trapped inside a bankrupt corporation.

The legal battle that followed went all the way to the Third Circuit U.S. Court of Appeals. The mineral owners made what sounds like a completely rational argument: local state laws gave them a protected trust right to the oil. They argued that the downstream buyers who ultimately got the crude should have to pay the royalty owners first.

The court sided with the big money.

The downstream buyers and the Wall Street banks had taken legal precautions to protect themselves in the event of SemGroup’s insolvency. The individual mineral owners had not. The court ruled that parties who take precautions do not act as insurers for those who take none. The banks got paid in full. The mineral owners were wiped out.

This case sent shockwaves through the industry. Legal scholars even began asking if midstream crude purchasers needed federal banking regulations to prevent them from gambling with producer money. But for the families who lost their royalties, the academic debates did not pay the bills.

Why the “It’s My Oil” Argument Fails

To understand how this happens, you have to look at the chain of custody.

When you sign a lease and the operator drills a well, you are entitled to a share of the production. You probably remember signing paperwork to set this up. We wrote about Understanding Your Division Order recently, which is the document that tells the purchaser exactly what decimal interest you own.

The problem starts the second the oil passes the wellhead meter.

Once that oil enters the pipeline network, it physically mixes with crude from hundreds of other wells. It becomes legally untraceable. If the purchaser goes bankrupt holding that oil, you cannot walk into the storage tank and scoop out your specific barrels.

At that exact moment, your physical property right converts into a financial account receivable. You no longer own oil. You own an IOU from a corporation.

If that corporation files for Chapter 11, federal bankruptcy law takes over. In the eyes of a bankruptcy judge, you are no different than the vendor who sold the bankrupt company office paper, or the janitor they hired to clean their headquarters. You are an unsecured creditor. The secured creditors—usually the massive banks that lent the company operating capital and filed formal liens against all of the company’s assets—get to eat first.

Usually, by the time the banks are done eating, there is nothing left on the table for the families.

The Border War Between State Laws

After the oil busts of the 1980s, producing states knew this was a problem. Both Texas and Oklahoma tried to protect their local mineral owners by passing laws designed to give them a security interest in the oil they sold.

But the SemCrude bankruptcy proved that one of those states wrote a bad law.

Texas relies on Section 9.343 of its Business and Commerce Code, commonly known as a :first purchaser statute. It says that an interest owner automatically gets a security interest to secure payment. It sounds great on paper. You don’t have to file any confusing UCC financing statements. The law just protects you.

There is a fatal flaw in the Texas law.

Under the Uniform Commercial Code, the law that governs a security interest is based on where the debtor is legally located, not where the oil comes out of the ground. Most of these midstream purchasers are Delaware LLCs or Delaware LPs. SemCrude was a Delaware entity. Because the debtor was “located” in Delaware, the federal court looked at Delaware law. Delaware does not have an automatic protection statute for Texas mineral owners.

Because the Texas mineral owners relied on the flawed Texas statute instead of filing manual liens in Delaware, their claims were thrown out. Texas owners lost everything.

Oklahoma faced the exact same problem in the SemCrude case. Their old 1988 law failed for the same reasons. But unlike Texas, Oklahoma actually fixed it.

The Oklahoma legislature passed the Oil and Gas Owners’ Lien Act of 2010. They changed the fundamental nature of the protection. Instead of creating a commercial security interest, they created a real property lien that is tied directly to the physical dirt in Oklahoma. The 2010 Act specifically says the governing law is the state where the oil and gas rights are located, bypassing the whole Delaware loophole.

Under Oklahoma Statutes Title 52, Section 52-570.10, revenue is explicitly supposed to be held for the benefit of the owners legally entitled to it.

Did the Oklahoma fix actually work? We found out recently.

A few years ago, another midstream buyer called First River Energy, a Delaware LLC, filed for bankruptcy. They owed money to both Texas and Oklahoma producers. The Texas Bar closely tracked the outcome.

The judge looked at the Texas producers and gave them the exact same bad news as the SemCrude case. The Texas statute failed because First River was a Delaware company.

But when the judge looked at the Oklahoma producers, the 2010 Act held up. The court recognized that Oklahoma had successfully created a superior property lien. The Oklahoma producers were protected. The Texas producers were not.

As of right now, the Texas legislature still has not rewritten its law to fix the loophole. If you own minerals in Texas and your purchaser goes bankrupt in Delaware, you are exposed.

The Reality of Tail Risk

I want to be clear about the math here. A midstream purchaser going bankrupt is not an everyday occurrence. Most months, the oil flows, the purchaser pays the operator, and the operator cuts your check.

But this is what financial people call “tail risk.” It is an event with a relatively low probability of happening on any given Tuesday, but if it does happen, the financial devastation to your family is absolute.

We see families who inherit fractional mineral interests. They get a check for $800 or $2,000 a month. They look at that check and think of it as a permanent annuity. They budget around it. They use it to pay their property taxes or put their kids through college.

They don’t realize that their “annuity” relies on a complex chain of custody involving operators, midstream marketers, and downstream refineries. If a single link in that chain decides to gamble on the futures market and loses, the family’s annuity vanishes overnight. We covered similar structural risks in The Royalty Black Hole: Why Your Checks Stopped (But the Well Didn’t).

You can do everything perfectly. You can negotiate a great lease. The geology can be fantastic. The operator can do a brilliant job completing the well. And you can still end up with nothing because a corporate entity in Delaware collapsed under its own debt.

This is the exact reason many small and fractional mineral owners ultimately decide they do not want to be in the oil and gas business.

The emotional weight of holding onto family land is real. We respect it completely. But we also see the reality of what happens when these obscure legal mechanisms fail the little guy. A family office or an institutional buyer has the capital to absorb a SemCrude-style bankruptcy. We spread our risk across thousands of wells and hundreds of purchasers. If one purchaser blows up, it hurts us, but it doesn’t bankrupt us.

If you are a family holding a single tract of land, you do not have that luxury. Your risk is concentrated. If your purchaser goes down, your entire income stream goes down with it.

Deciding what to do with an inheritance is complicated. We wrote a broader piece on this called Should I Sell My Mineral Rights? A Guide for Families because we know how hard these conversations are.

Selling is just one option. But it is an option that completely removes counterparty risk from your life. You trade the uncertainty of the pipeline system for cash in the bank, and you let whoever buys your minerals worry about Delaware bankruptcy law.

If you are tired of wondering what liabilities are lurking behind your monthly royalty check, it might be worth a conversation to see what your minerals are actually worth right now. You might look at the number and decide to keep them. But you should at least know your options, and you should definitely know the risks you are currently carrying for free.

:first-purchaser

The company that actually buys the raw oil or gas as it comes out of the wellhead. They are the initial link in the financial chain, taking physical possession of the hydrocarbons and introducing the first layer of payment risk into your royalty check.

:unsecured-creditor

A person or company owed money by a bankrupt entity, but who has no specific collateral or legal lien guaranteeing payment. In a bankruptcy proceeding, unsecured creditors are at the very back of the line and frequently receive nothing.

:first-purchaser-statute

State laws designed to automatically give mineral owners and operators a legal claim against the companies buying their oil. As the SemCrude case showed, these laws often fail in federal bankruptcy court if they are poorly written.